TOPIC 3 CONTROLLING

types of organizational control

Control, or controlling, is one of the managerial functions like planning, organizing, staffing and directing. It is an important function because it helps to check the errors and to take the corrective action so that deviation from standards are minimized and stated goals of the organization are achieved in a desired manner.

According to modern concepts, control is a foreseeing action whereas earlier concept of control was used only when errors were detected. Control in management means setting standards, measuring actual performance and taking corrective action.

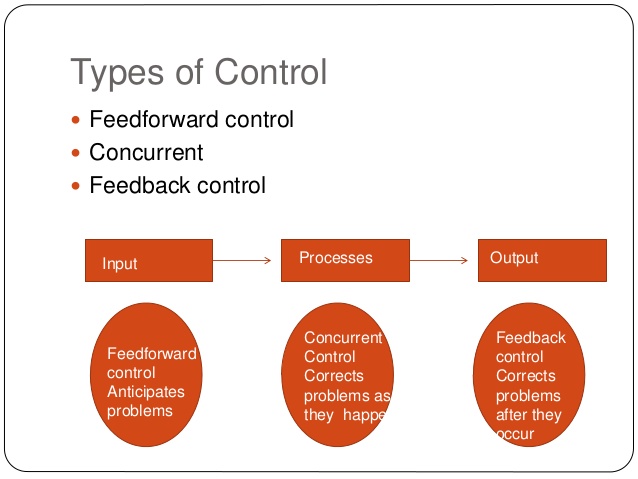

Feedforward controls

sometimes called preliminary or preventive controls, attempt to identify and prevent

deviations in the standards before they occur. Feedforward controls focus on human,

material, and financial resources within the organization. These controls are evident in the

selection and hiring of new employees. For example, organizations attempt to improve the

likelihood that employees will perform up to standards by identifying the necessary job skills

and by using tests and other screening devices to hire people with those skills.

Concurrent controls

monitor ongoing employee activity to ensure consistency with quality standards. These

controls rely on performance standards, rules, and regulations for guiding employee tasks

and behaviors. Their purpose is to ensure that work activities produce the desired results.

As an example, many manufacturing operations include devices that measure whether the

items being produced meet quality standards. Employees monitor the measurements; if they

see that standards are not being met in some area, they make a correction themselves or

let a manager know that a problem is occurring.

Feedback controls

involve reviewing information to determine whether performance meets established

standards. For example, suppose that an organization establishes a goal of increasing its

profit by 12 percent next year. To ensure that this goal is reached, the organization must

monitor its profit on a monthly basis. After three months, if profit has increased by 3 percent,

management might assume that plans are going according to schedule.

source:https://www.google.com/search?source=hp&ei=irTrWo7mMYyBvwShnLuYCQ&q=type+of+controlling+in+management&oq=type+of+controlling&gs_l=psy-ab.1.1.0l4j0i22i30k1l6.6486.55258.0.73212.66.43.22.0.0.0.155.2801.41j1.43.0....0...1.1.64.psy-ab..1.65.3147.6..46j35i39k1j0i67k1j0i10k1j0i13k1j0i13i30k1j0i13i10i30k1j0i131k1j0i131i67k1j0i46k1j0i20i263k1.60.x0jvxf8U6Es

Comments

Post a Comment